Have you ever set some financial goals only to give up after several weeks? Maybe you have started budgeting and had good intentions to improve your financial stability but considered it too restrictive and gave it up.

We all know that budgeting and financial planning needs sacrifices and dedication. Without setting meaningful monetary goals and a strict budgeting strategy you won’t get too far. Here is how to set and achieve financial goals for a hopeful future.

The Definition of Financial Goals

What are financial targets? They are money-related goals a person wants to achieve. For instance, you may want to save $1,000 a month or earn six figures per year. Besides, financial objectives can mean goals that require money to achieve.

For instance, you need to save or borrow money to purchase a house or an auto or go on a long-awaited vacation.

By determining something you want to purchase, experience, or pay for, you may come up with a definite plan to obtain the funds it requires. Your financial target is the monetary aim. There are two kinds of financial goals you may set and achieve:

Near-term targets: These are the goals you would like to get sooner. Short-term aims should be achieved within one year or even less. For instance, you may want to repay instant cash loans you’ve taken to cover urgent medical bills.

Long-term targets: These are the goals you would like to get within several years or decades. They demand you to take a step back and make smaller steps or milestones until you reach them. For instance, you may want to get a mortgage to buy a house or establish a retirement fund.

How to Set Financial Goals

Where should you begin if you decide to set financial goals? If these targets don’t align with your real desires and wishes, chances are that you won’t stick with them and will eventually give up on them.

Of course, now there are many popular money borrowing apps that you can use right now and cover your momentary desires. But it is better to correctly calculate your short-term and long-term financial targets and be confident in your financial future.

Take some time to think about your real wishes and dreams. Imagine your perfect life and the things you want to achieve. Don’t rush with your decisions as you will need to remain consistent and motivated for a long time to reach your targets.

Where do you want to live? What do you want to own? What would you like to experience? What do you want your future to look like?

Every person may have different aspirations so ask yourself these questions and remember to be honest with yourself. Your financial goals may depend on several factors including the place and cost of living, the people you would like to live with, etc.

The Current Situation with Personal Finances

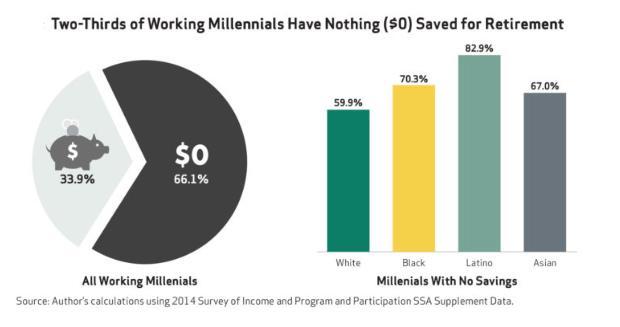

Thousands of Americans struggling with their finances these days. The survey shows that 95% of millennials are saving less than the recommended amount.

If you don’t have a solid emergency fund and neglect the state of your household finances, the problems may become even worse.

The main difference between those in a financially secure position and those struggling to make the ends meet comes down to these few things: resourcefulness, planning, and literacy. While 34% of all Americans have zero savings at all, 83% of consumers who set financial goals feel better about their finances after just one year.

Examples of Short-Term Goals

- Travel;

- Wedding;

- Emergency fund;

- Payments toward student loans, insurance, rent;

- Credit card debt payments;

- Home renovations and minor repairs.

Examples of Mid-Term Goals

- Paying off debt;

- Saving for a down payment;

- Purchasing an auto.

Examples of Long-Term Goals

- Starting a business;

- Retirement fund;

- Saving for a child’s college tuition;

- Repaying a mortgage.

How to Budget and Save for Short-Term and Long-Term Goals

You need to prioritize your financial targets. Most people will likely have a combination of near- and long-term financial aims to balance. Concentrate on your basic needs and general expenses first.

If you see you have enough funds left, you may set some goals such as establishing a retirement and an emergency fund. It should be one of your priorities.

It’s essential to have a solid emergency fund to protect you from unforeseen situations. Different obstacles can easily unsettle you, but if you have some cash set aside, the monetary emergency won’t distract you from reaching your financial aims.

Define how much income you have and how much you spend each month. This is the basis of your budget as you need to know where you stand. A great option is to utilize the 50/30/20 budget calculator in the beginning.

You will allocate 50% of your income toward “needs”, and 30% of your profit toward “wants”, and leave the rest 20% for savings and debt repayment. Try your best to lower monthly spending as it may adversely affect your ability to achieve financial goals.

Whatever money is left over at the end of the month should go into your savings account to help you reach your targets faster.

Where to Save for Your Financial Goals

You also need to find a safe place where you can keep your funds until you finally need them to purchase the desired item or finance your aim. For near-term goals and emergency funds, you will need to keep your funds in a place you can gain access fast.

It can be your savings account, for example as you won’t have any penalties for using it. As for long-term goals, it’s better to put your money aside into a certificate of deposit or a savings account.

The certificate of deposit with a high-interest rate will help you obtain more money within several years if you aren’t planning to use it sooner.

The Bottom Line

To sum up, those who want to set and achieve their financial goals should set a budget, lower their monthly spending, and save as much as they can. Focus on your real aims and the things you want to achieve in life.

Prioritize your goals and set short-term and long-term monetary targets. Establish an emergency fund and a savings account where you will set your cash aside.

{kind=link}